Straight Talking IVAs

Learn everything you need to know about IVAs in our straight-talking guide.

So what exactly is an Individual Voluntary Arrangement (IVA)?

An IVA is a legally binding agreement between you and the people you owe money to. You will be expected to pay what you can realistically afford each month (after living costs have been accounted for), usually for a period of five years and in return your creditors will agree to freeze interest and write-off any outstanding debt at the end of the arrangement. Typically, an IVA will write off between 50% and 60% of an average debt of just under £60,000.

So are there fees to pay in an IVA?

Everyone who provides and manages an IVA – charities like ourselves or commercial organisations, receives a fee out of the money you pay to your creditors (the people you owe money to). Your creditors agree to a fee for setting up the IVA, which is a legal agreement, and then for managing the IVA, typically for a period of five years. We all receive the same payments to do this. The important thing is to make sure that you get impartial advice on whether an IVA is right for you and if it is, that you don’t pay any unnecessary upfront fees.

So what do you pay?

It doesn’t matter how much your current monthly payments are, you will only be expected to pay what you can reasistically afford into the IVA, which is the amount you have left over after your essential monthly outgoings have been accounted for. You may also be required to release some of the equity that is available in your home at the end of the IVA – but only if you can afford to (in some circumstances, if you are unable to remortgage, then you may be asked to carry on making payments for a further 12 months – see IVA Remortgage).

This reduced repayment figure is offered to your creditors in the form of an IVA proposal. At least 75% of your creditors (by amount of debt, not number of creditors) have to accept the proposal in order for the IVA to be approved.

So for example, if you owed £25,000, you did not own your own home and you could only afford to offer your creditors £200 a month (after your day to day living costs have been accounted for), then assuming your creditors agree, you’ll pay back £12,000 in total over the sixty months (this includes your Insolvency Practitioner’s fee), which means that £13,000 is then written off. Technically, you have written off more than £13,000 because part of the £12,000 you paid into the IVA went towards fees. Very broadly, your creditors will receive around 80% of the total amount you pay into your IVA with your IP receiving the other 20%. You can read more about IVA fees here.

So is the IVA free?

If your IVA application is approved, the amount you can afford to pay each month (as well as any available equity) is the only amount you will pay – you don’t have to pay a fee on top.

Your creditors agree that the IVA provider (charity or commercial company) takes their fee from each payment they receive from you, with the balance being passed on to your creditors.

Because the total amount you pay back during the IVA is likely to be significantly less than the original amount of debt you had, you’ll sometimes see the IVA described as free to the consumer. Whilst this view is understandable (how can you have a negative fee), it’s still important that you understand fees are involved for two important reasons; in case you benefit from a significant windfall during your IVA or in case your IVA fails (see who pays the IVA fees for more information).

So what if you can’t keep up with your IVA payments?

If you don’t stick to the monthly payments that you have agreed to then the IVA is said to be in default. If there’s a good reason why you’ve been unable to make your payments then your Insolvency Practitioner (IP) can talk to your creditors and renegotiate your monthly payments to get you back on track.

If your creditors are not prepared to accept that the reasons you’ve given for failing to keep up with your payments are justified then they may require your IP to fail your IVA.

If your financial circumstances change we will do our very best to negotiate a payment restructure on your behalf. Remember, it’s nearly always in your creditors’ best interests to accept whatever payments you can afford to make as the they are unlikely to recieve as much back if the IVA fails.

So what happens if my IVA fails?

If your IVA fails then your debts will be reinstated less any payments received by the creditors (this is the sum total of payments you’ve made up to that point less any fees your creditors have agreed to give your IP). Also, interest may be added back on and your IP may be required by your creditors to petition for your Bankruptcy. Individual creditors will also regain the right to petition for your Bankruptcy and you will be back to where you were before you agreed to the IVA.

An Insolvency Practitioner, whether they are employed by a charity or a commercial organisation, will get paid the same amount in fees – they are generally higher in the first six months of your IVA in recognition of the set up work carried out by your IP and then reduce to a percentage of the monthly payment thereafter. This means that should your IVA fail after only a few months, your debt is unlikely to have reduced by much. This is why we will only suggest an IVA to you if it suits your financial circumstances and you feel you can commit to living to an agreed expenditure for five years.

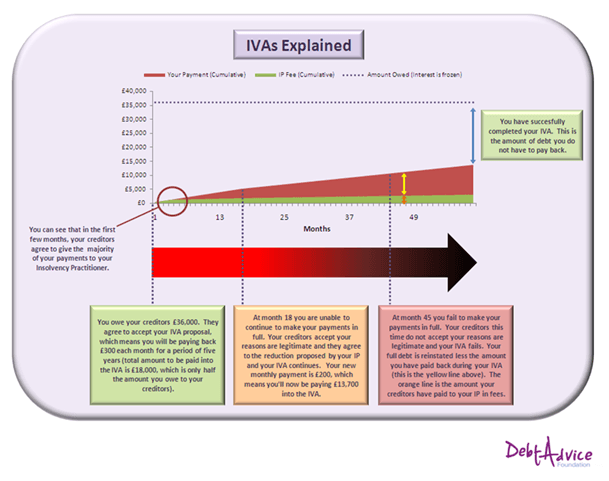

Click on the image below to see a larger version of how IVAs work in overview.

Will an IVA affect my credit rating?

An IVA will affect your credit rating as it will stay on your credit file for six years from the date your IVA passes (this is typically one year after your IVA has been completed).

Most people take the view that dealing with their debt problem is much more important than impairing their ability to take out further credit when they’re already in severe financial difficulty.

Does Debt Advice Foundation provide IVAs?

Yes we do. As a registered UK charity we provide free debt advice to anyone who contacts us and we only recommend the solution that is right for each individual based on their circumstances. Our range of solutions extends from self help guidance through to non-fee charging DMPs, DROs, IVAs and Bankruptcy.

If you need to talk confidentially to someone about debt, there’s no need to wait or book an appointment, our Advisors are available Monday to Friday 8am to 6pm.